Home Equity Loans vs. Equity Loans: Understanding the Differences

Home Equity Loans vs. Equity Loans: Understanding the Differences

Blog Article

Secret Factors to Take Into Consideration When Applying for an Equity Car Loan

When thinking about applying for an equity finance, it is crucial to navigate via different essential factors that can dramatically affect your financial health. Recognizing the types of equity finances readily available, evaluating your qualification based on monetary factors, and thoroughly analyzing the loan-to-value proportion are necessary first actions.

Sorts Of Equity Loans

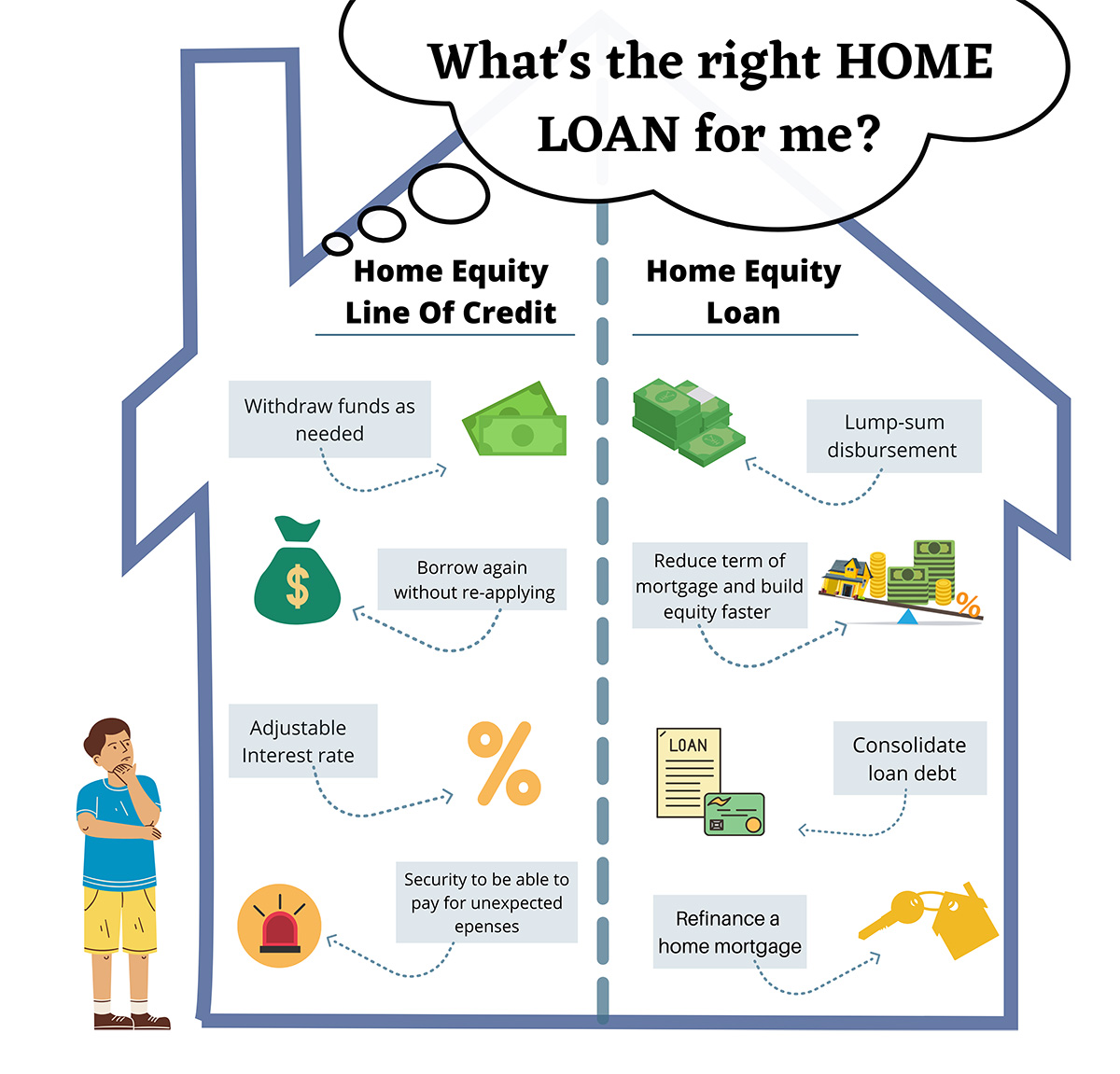

Numerous financial institutions supply a series of equity financings tailored to satisfy varied borrowing requirements. One usual kind is the standard home equity financing, where home owners can borrow a swelling amount at a set rates of interest, utilizing their home as security. This kind of loan is suitable for those who require a large amount of money upfront for a specific function, such as home improvements or financial obligation combination.

One more prominent choice is the home equity line of credit report (HELOC), which works extra like a bank card with a revolving credit score restriction based upon the equity in the home. Borrowers can draw funds as required, approximately a certain limit, and only pay rate of interest on the quantity used. Home Equity Loans. HELOCs are appropriate for continuous expenses or projects with uncertain prices

Furthermore, there are cash-out refinances, where home owners can re-finance their existing home mortgage for a higher quantity than what they get the distinction and owe in cash - Alpine Credits Equity Loans. This sort of equity car loan is helpful for those seeking to make the most of lower rates of interest or gain access to a big sum of money without an additional regular monthly settlement

Equity Financing Qualification Aspects

When taking into consideration eligibility for an equity lending, banks commonly analyze aspects such as the applicant's credit rating, revenue stability, and existing financial debt responsibilities. An essential facet is the credit history, as it shows the customer's credit reliability and capacity to settle the loan. Lenders choose a greater credit history score, typically above 620, to mitigate the danger associated with lending. Earnings stability is another key variable, showing the borrower's ability to make regular finance settlements. Lenders might call for proof of consistent income with pay stubs or income tax return. In addition, existing debt obligations play a considerable duty in determining qualification. Lenders assess the borrower's debt-to-income ratio, with reduced proportions being a lot more positive. This proportion suggests just how much of the consumer's income goes towards paying back financial debts, influencing the lender's choice on funding authorization. By thoroughly examining these variables, banks can figure out the candidate's eligibility for an equity financing and develop suitable car loan terms.

Loan-to-Value Proportion Considerations

A reduced LTV proportion indicates much less risk for the lending institution, as the consumer has more equity in the residential property. Lenders normally like lower LTV proportions, as they provide a better pillow in situation the consumer defaults on the financing. A greater LTV proportion, on the other hand, recommends a riskier investment for the lender, as the consumer has less equity in the residential property. This might lead to the lending institution imposing higher rates of interest or more stringent terms on the lending to mitigate the raised risk. Customers must intend to maintain their LTV proportion as reduced as feasible to enhance their possibilities of approval and protect a lot more positive lending terms.

Rate Of Interest Prices and Charges Contrast

Upon examining rate of interest rates and costs, customers can make informed choices concerning equity fundings. When comparing equity loan alternatives, it is necessary to pay close interest to the interest prices offered by various loan providers. Interest prices can substantially impact the overall price of the funding, affecting month-to-month repayments and the total amount paid off over the car loan term. Reduced passion rates can lead to substantial savings gradually, making it important for customers to search for the most affordable rates.

Apart from passion prices, consumers should likewise think about the numerous costs associated with equity lendings. Early repayment charges may apply if the debtor pays off the financing early.

Repayment Terms Assessment

Reliable evaluation of payment terms is critical for borrowers seeking an equity financing as it directly impacts the finance's affordability and monetary end results. The lending term refers to the length of time over which the customer is expected to pay off the equity financing. By extensively evaluating repayment terms, borrowers can make informed decisions that align with their financial objectives and guarantee successful funding monitoring.

Verdict

Finally, when making an application for an equity loan, it is necessary to think about the kind of funding offered, qualification aspects, loan-to-value proportion, rates of interest and fees, and repayment terms - Alpine Credits Canada. By meticulously reviewing these vital factors, borrowers can make informed decisions that align with their financial objectives and conditions. When looking for an equity funding., it is vital to completely research and contrast choices to guarantee the best feasible result.

By thoroughly assessing these factors, economic establishments can establish the applicant's eligibility for an equity financing and develop appropriate lending terms. - Equity Loans

Interest prices can substantially continue reading this impact the total expense of the funding, affecting month-to-month settlements and the total quantity paid back over the lending term.Reliable analysis of payment terms is essential for customers looking for an equity funding as it directly influences the funding's affordability and monetary outcomes. The loan term refers to the size of time over which the borrower is anticipated to pay off the equity finance.In final thought, when applying for an equity loan, it is crucial to consider the kind of financing readily available, qualification elements, loan-to-value proportion, rate of interest rates and costs, and settlement terms.

Report this page